NRI Repatriation & FEMA Guide 2026

repatriating funds from Indian property sales requires clearing capital gains taxes and complying with RBI's annual USD 1 Million LRS caps. This guide maps FEMA bank compliance codes and Form 15CA/15CB processes.

Key Highlights covered:

- Remittance Caps: Rules for transferring funds up to USD 1 Million per year from NRO accounts.

- Form 15CA/15CB: Step-by-step tax declaration filing with CA certification.

- Property gains: Tax deductions, TDS exemptions, and lower tax certificate filings.

- FEMA declarations: Bank report codes and inward remittance reporting structures.

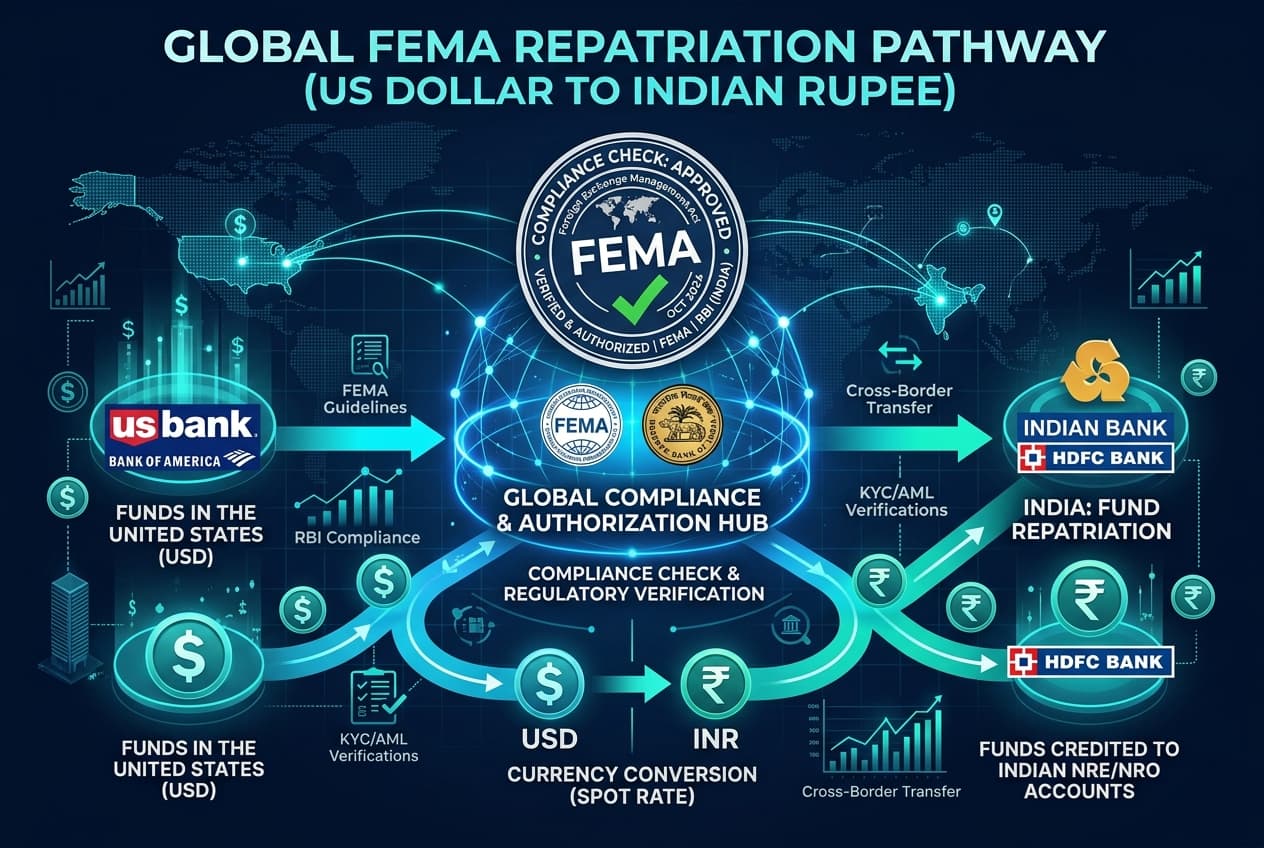

What is the process for repatriating property sale funds?

The buyer typically deducts TDS at 20%+ on the property sale price. The NRI must secure a tax clearance certificate (Form 15CA) and a CA audit report (Form 15CB) certifying that appropriate taxes have been paid, before the AD bank executes the outward foreign exchange remittance.

How is the USD 1 Million FEMA annual limit tracked?

AD Category-I banks track remittances under the NRO account route, validating that the total funds repatriated by the NRI out of India across all banks do not exceed USD 1 Million per financial year.

Frequently Asked Questions

India has no inheritance tax, so inheriting assets is tax-free. However, any income generated from those assets (like rent or interest) or capital gains from selling them are taxable, requiring Form 15CA/15CB filings for remittance.

Need professional assistance?

Our qualified partners can advise you directly on corporate taxation, FEMA certifications, and company formations.

This article is written and reviewed by practicing Chartered Accountants of DSS Corp Advisory in Chennai. Information is aligned with the latest Finance Act notifications.